Omdia: AI Factory market enters industrialization era as five dynamics redefine AI infrastructure in 2026

LONDON, May 28, 2026: Cumulative global data center investment is forecast to approach $1.6 trillion by 2030, while leading technology enterprises will collectively deploy over $600 billion in AI infrastructure capex in 2026 alone. This capital expenditure indicates that the AI Factory market has crossed an irreversible threshold, evolving into a new form of industrial organization characterized by ultra-high capital intensity, strong geopolitical attributes, and complex engineering barriers.

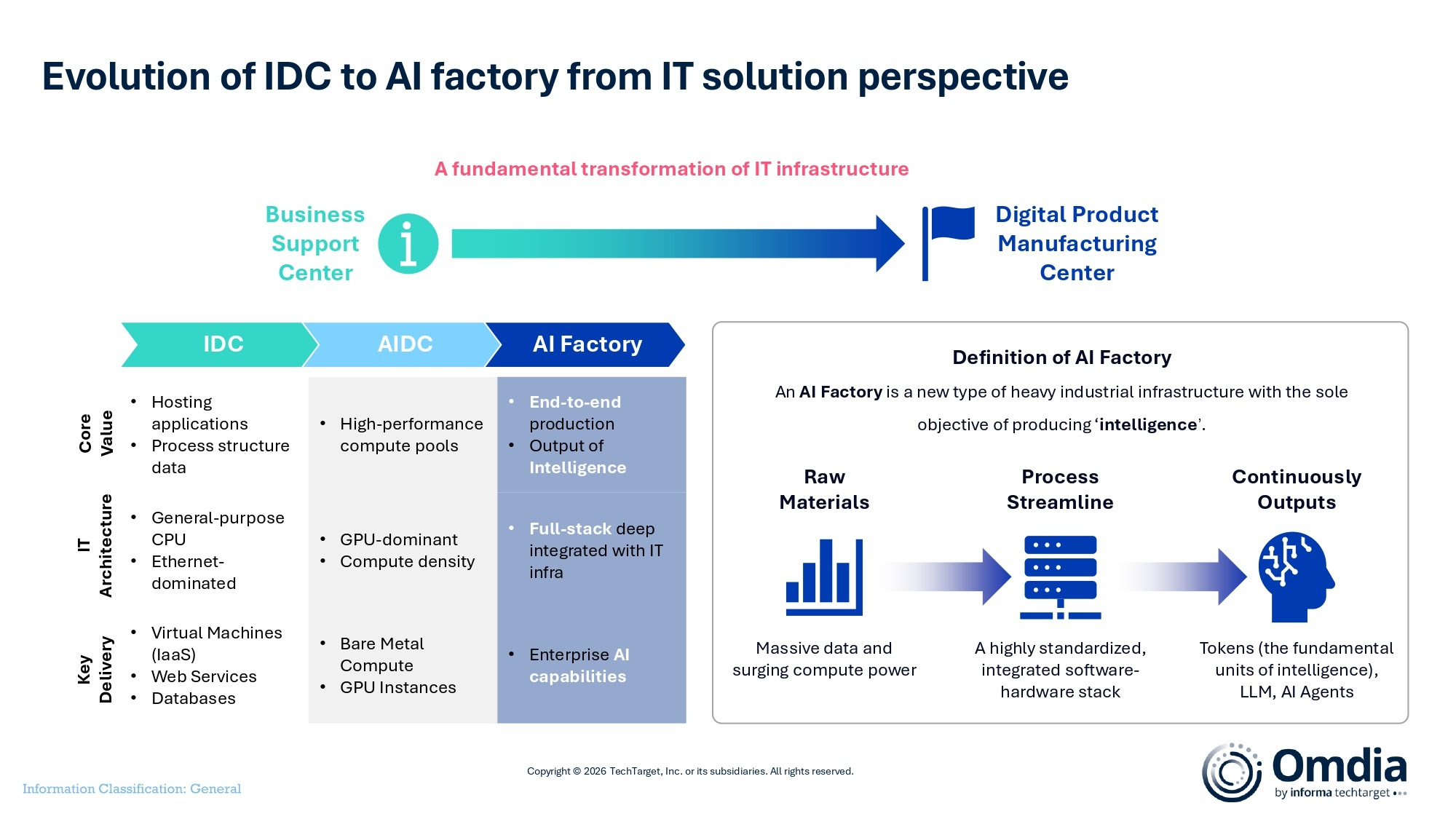

The Transition to AI Factory: Architecture and Paradigms

Omdia defines an AI Factory as a new type of heavy industrial infrastructure whose sole objective is producing intelligence, with the token as the fundamental unit of output. data centers are transitioning from business support centers to digital product manufacturing centers no matter how big the data center is, organized along a four-layer architecture: energy and physical infrastructure; hardware and network fabric; scheduling and virtualization orchestration; and Model as a Service (MaaS) and AI application ecosystem.

The ecosystem now spans four solution paradigms—full-stack public AI cloud hyperscalers, compute-native AI cloud specialists, turnkey private AI foundation providers, and regional or industrial AI infrastructure operators. Omdia’s survey of more than 200 companies identifies four top market challenges: long time-to-market and ROI validation, digital sovereignty, AI talent gaps, and systemic engineering complexity.

Five Market Dynamics Shaping AI Factory in 2026

As the market navigates these challenges, Omdia has identified five primary dynamics reshaping the industry this year:

- Dynamic 1 — From FLOPS to TTFT: Budgets for compute hoarding have been frozen as enterprises confront a “Zombie GPU” effect, in which expensive GPUs idle in I/O wait; evaluation metrics are shifting to Time-to-First-Token and vector retrieval speed, with reported gains, including a 12x vector indexing speed-up and up to a 75% cost reduction on API and compute redundancy in vendor case studies.

- Dynamic 2 — Hyperscalers balance agility and sovereignty: Two delivery paradigms: one is called full-stack drop-in (AWS, Huawei, GCP, OCI) enable public cloud-grade AI capabilities deployed as an integrated physical unit into the customer’s data center; another one is called software/hardware decoupling which is a downward path defined by localization of software capabilities and ecosystem-driven hardware

- Dynamic 3 — Compute-native AI cloud upgrade: Rack power density has risen from 10–15 kW in 2024 to 40–250 kW in 2026, while workloads progress from PoC to production-grade deployment; Nebius from Europe and Sensetime from China are two typical players already changed their business model from Bare Metal leasing to Model as a Service, especially Sensetime is conducting an integrated framework of IaaS + MaaS + energy-computing synergy strategy to make the computing and energy well controlled

- Dynamic 4 — The “last mile” of AI industrialization: Vertical integrators, domain operators, and ISVs are capturing the final value layer through long-cycle data governance, legacy integration, and scenario-specific agent assembly, while Inspur Cloud takes a strategy integrated heavy-asset AI infrastructure and intensive scenario-grade operation of AI industrial assembly lines making the AI industrialization a great leap.

- Dynamic 5 — Rise of sovereign data factories: Regulatory frameworks such as the EU AI Act, DORA, and equivalent compliance frameworks are driving requirements for sensitive data to remain within physically isolated facilities, elevating regional operators such as G42 from cabinet landlords to physical gatekeepers of national-level data.

“Future competition will no longer be defined by model parameters or GPU counts, but by a comprehensive contest of energy, liquid cooling, chips, autonomous software stacks, sovereign compliance, and long-term capital endurance,” said Raymond Zhan, Senior Principal Analyst, Cloud & AI at Omdia. ” For enterprise clients, the provider landscape for AI factory is not a one-size-fits-all game; choices should be tailored to actual business scale and the balance between steady-state and innovative workloads.”

Looking ahead, Omdia expects 2026 and 2027 to be the critical window for AI Factory development, with regional and industrial operations emerging as the highest-certainty growth segment over the next five years.

Omdia’s Global AI Factory Market Landscape 2026 report provides a comprehensive analysis of the AI Factory market, including detailed architectural frameworks, solution paradigms, and insights into the key dynamics shaping AI infrastructure.